"A ship in harbor is safe, but that is not what ships are built for."

— John A. Shedd

This saying usually gets attributed to American author and professor John A. Shedd and is an excellent illustration of the connection between risk and opportunity.

We understand that keeping a ship in the harbor can protect it from storms, pirates, and accidents at sea. But a ship wasn't built to sit idle. It was built to sail, explore and transport.

What Shedd is really telling us is that playing it safe can prevent us from achieving our true potential. Life, work, and personal growth all involve elements of risk taking. Attempting to avoid risk often means missing out on life's greatest rewards.

But what if we can find ways to manage risks to acceptable levels, so that we can still pursue our goals and desires? What other exciting and rewarding opportunities could we achieve in our lives? Identifying, understanding and appropriately managing risks in order to achieve goals is the true essence of risk management.

This guide will explain the key foundational concepts of risk management from a business perspective. The guide will focus on enterprise risk management (ERM), but all of the ideas and principles can be easily applied to other forms of risk management as well.

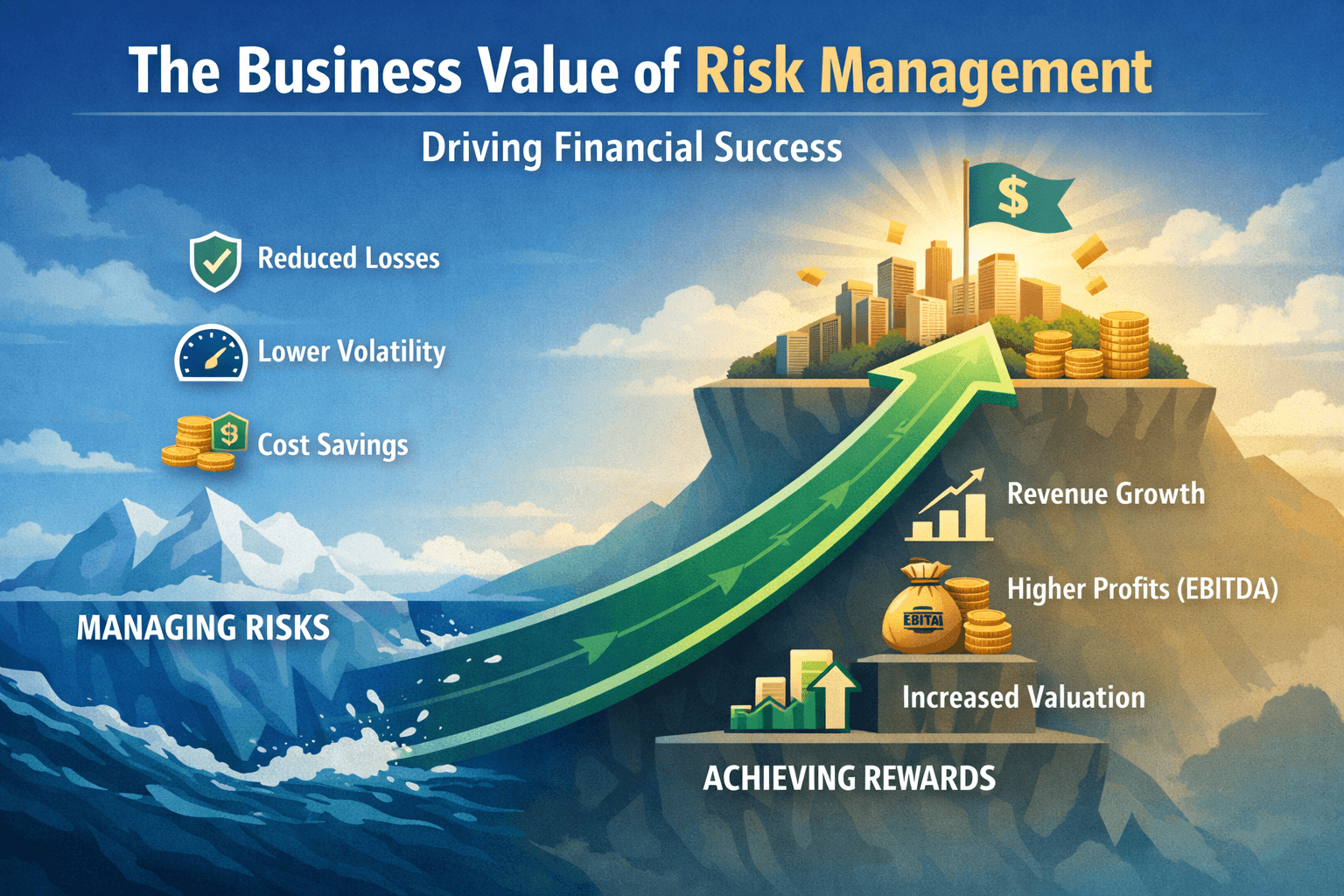

2. The Business Value of Risk Management

Risk management in the business world is a big deal. Embracing risk and the practice of risk management leads to clear rewards, as illustrated by numerous studies.

For example, an Ernst & Young study conducted 576 interviews and reviewed 2,750 company and analyst reports. They found that companies with more mature risk management practices outperformed their peers in key financial metrics, including higher revenue growth, higher earnings (EBITDA) and higher earnings yields.

These companies weren't simply using their mature risk management practices to avoid all risks—rather, they were using their mature practices to assume smart risks and manage risks better so they could achieve their business goals with more certainty.

Similarly, Eckles, D., Hoyt, R. and Miller found that practicing Enterprise Risk Management led to lower costs, reduced volatility in financial performance, and higher operating profits for comparable levels of risk.

Farrell and Gallagher found that firms with high ERM maturity—not just basic or check-the-box risk processes—show significantly higher market valuations (about 25% higher, on average, all else being equal). The biggest driver of this value wasn't better risk registers or tools, but strong executive leadership and a risk-aware culture that flows from the top throughout the organization. When ERM is actively used in strategy decisions and day-to-day operations, companies are better at spotting how risks interact across the enterprise, and markets reward that capability with higher firm value.

In research that's very relevant in 2026, the Aon Risk Maturity Index (RMI) found that organizations with more mature risk management practices consistently perform better and are more resilient in times of uncertainty. They have stronger stock price performance, lower share price volatility, and higher market valuations. These organizations also respond more resiliently to major external shocks and benefit financially through lower Directors & Officers insurance premiums.

Together, these studies and many others demonstrate that embedding risk management into strategy, governance, and day-to-day decision-making improves stability, strengthens performance, and creates tangible financial value over time.

3. What are Risks?

Let's get back to our "101" approach and start from the beginning—what are risks?

If you look in Webster's dictionary you'll find a definition that describes a risk as the "possibility of loss or injury" or "something that creates or suggests a hazard."

Those definitions aren't wrong. In fact, they're useful in certain contexts—insurance, safety, or emergency response, for example. But they also help explain why the word "risk" often carries such a negative emotional charge. If risk is always framed as danger, loss, or harm, it's no surprise that people instinctively want to avoid it, minimize it, or push responsibility for it onto someone else.

In business, however, that narrow view of risk quickly becomes limiting. It leads to risk being treated as a compliance exercise, a reporting obligation, or a list of things that must be prevented at all costs. When risk is only about "bad things happening," organizations tend to focus on defensive controls, box-checking, and avoiding blame—rather than making better decisions.

A more practical and helpful way to think about risk in a business context is this:

A risk is an uncertain event or condition that could affect our ability to achieve our objectives.

This definition intentionally removes the assumption that risk is always negative. Some risks may indeed lead to losses or setbacks, but others may create opportunities e.g. new markets, efficiencies, innovations, or strategic advantages. What they all have in common is uncertainty and impact on outcomes that matter.

Seen this way, risk is not something separate from strategy or operations—it is embedded in them. Every meaningful business decision involves uncertainty: launching a new product, entering a new market, investing in technology, changing suppliers, or responding to regulatory change. Risk management, therefore, is not about eliminating uncertainty (which is impossible), but about understanding it well enough to make informed choices.

This shift in definition is subtle but powerful. It reframes risk management from a backward-looking exercise focused on past failures to a forward-looking discipline focused on future results. Instead of asking, "What could go wrong?" organizations can ask, "What could affect our success—and how prepared are we?"

In practice, this is where modern enterprise risk management adds value. By linking risks directly to goals, priorities, and decisions, organizations can focus their attention on the uncertainties that truly matter—those that could meaningfully influence performance, resilience, and long-term value.

4. The Four Main Categories of Risk

While every organization faces a unique mix of risks, most business risks fall into four broad categories. These categories help simplify complex risk landscapes and ensure important risks are not overlooked.

- Strategic risks relate to the choices an organization makes about its direction, goals, and competitive position. These risks influence long-term success and often involve significant uncertainty.

- Operational risks arise from the way an organization runs its day-to-day activities. They affect reliability, efficiency, and the organization's ability to deliver products and services consistently.

- Financial risks affect an organization's financial performance and stability, including revenue, costs, cash flow, and access to capital.

- Compliance and legal risks stem from laws, regulations, standards, and contractual obligations. These risks can threaten an organization's license to operate and damage trust with stakeholders.

In practice, organizations often find it more useful to keep a small number of high-level risk categories and introduce sub-categories beneath them, rather than continually adding new top-level categories. Too many primary categories can create confusion, overlap, and artificial silos, making risks harder to compare and prioritize. Sub-categories allow organizations to reflect their specific context (such as cyber, ESG, AI, or geopolitical risks) while still maintaining a clear, consistent enterprise view that supports integrated decision-making and avoids fragmenting risk ownership.

5. The Risk of the Status Quo in 2026

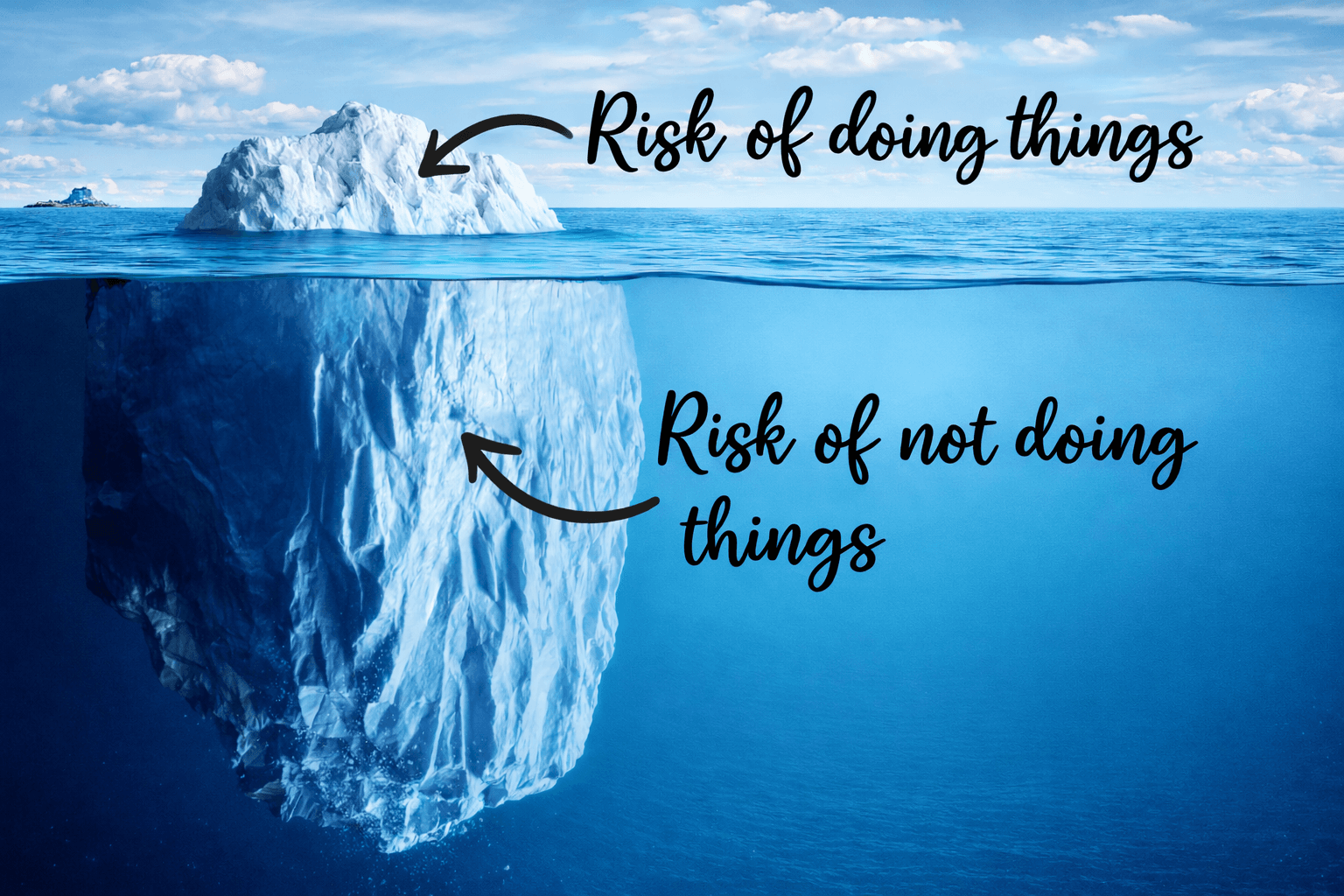

Many of us tend to think of risks as a byproduct of doing something. Driving a car. Making an investment. Launching a new product. Operating an assembly line. Entering new markets. Running with scissors. All of these actions can lead to the risk of bad things happening.

Often, however, risk comes from not doing something. Going back to Shedd's earlier analogy, leaving a ship in the harbor appears to be a good way to avoid risk. But what if you found out that a massive hurricane was going to hit the harbor? It's counterintuitive, but leaving harbor might actually be the safer option. In practice, many commercial ship captains will sail out into deeper waters, where they can maneuver, adjust course, and ride out the storm, rather than being smashed against docks, other vessels, or shore infrastructure. In other words, what looked like the safest option—staying put—can quickly become the most dangerous one when conditions change.

This is the essence of status quo risk: the risk that comes from standing still while the world around you moves.

In business, status quo risk is often overlooked because it doesn't feel like "taking a risk." There's no bold decision, no visible leap, and no immediate downside. Continuing to operate the same way you did last year feels safe, responsible, and prudent. But safety is relative. When customer expectations, technologies, competitors, regulations, and economic conditions are all evolving, doing nothing is still a decision—and often a risky one.

In 2026, this dynamic is more pronounced than ever. Organizations are operating in a period of rapid global transformation: artificial intelligence is reshaping how work gets done, supply chains remain fragile and geopolitically exposed, regulatory expectations are expanding, and competitive advantages are being created—and lost—at unprecedented speed. Business models that were stable just a few years ago can now become liabilities almost overnight.

The real risk many organizations face today is not that they will move too fast, but that they will move too slowly. Failing to modernize systems, rethink processes, invest in new capabilities, or adapt strategy can quietly erode resilience and relevance. By the time the consequences become obvious—lost market share, talent attrition, rising costs, or regulatory scrutiny—the organization's ability to respond may already be constrained.

Effective risk management doesn't push organizations toward reckless action, but it does challenge the assumption that the status quo is inherently safe. Just like a skilled ship captain, strong organizations continually assess changing conditions and adjust course accordingly. Sometimes the safest path forward is not staying in the harbor, but deliberately sailing into uncertainty—with eyes open, risks understood, and options prepared.

6. What is Risk Management?

We've mentioned the term risk management several times already, so let's take a moment and define it.

Once risks are understood in this way—as uncertainties that can affect objectives—the purpose of risk management becomes much clearer. Risk management is not about predicting the future or eliminating uncertainty. It is about making uncertainty visible, so leaders can make better, more confident decisions.

In a business context, risk management helps organizations clarify what they are trying to achieve, understand what could help or hinder success, and decide how much uncertainty they are willing to accept along the way. Done well, it supports thoughtful risk-taking rather than risk avoidance, and informed judgment rather than guesswork.

This is why modern risk management is increasingly viewed as a management discipline, not a control function. It connects strategy, operations, finance, and governance by asking practical questions such as: What matters most? What could materially affect it? And how prepared are we if things don't unfold as expected?

With this foundation in place, we can now turn to what risk management actually involves in practice—and how enterprise risk management (ERM) provides a structured way to apply these ideas across an organization.

7. What is Risk Appetite?

If risk management is about understanding uncertainty, risk appetite is about deciding how much uncertainty an organization is willing to accept in pursuit of its goals.

Put simply, risk appetite defines the boundaries within which leaders are comfortable operating. It answers questions such as: How much risk are we willing to take to grow? Where are we willing to push, and where do we want to be more cautious? What outcomes would be unacceptable, no matter the potential upside?

Going back to our ship analogy, risk appetite is not whether the ship sails or stays in harbor—it is how far it is willing to sail, in what conditions, and with what safeguards in place. Some organizations are comfortable crossing open oceans to reach new destinations. Others prefer shorter, well-charted routes. Neither approach is inherently right or wrong, but clarity is essential.

In a business setting, risk appetite helps translate strategy into practical guidance. An organization might have a higher appetite for innovation risk but a very low appetite for safety or regulatory risk. It might accept short-term earnings volatility to fund long-term growth, while having little tolerance for reputational damage. Without clearly articulated risk appetite, decisions tend to be inconsistent, reactive, or driven by individual comfort levels rather than shared intent.

In some cases, formalizing risk appetite may lead an organization to assume higher levels of risk. For example, an organization may be battling a culture of conservatism that is holding back their ability to innovate. They may also be spending more than they need to overcontrol risks that could be accepted at higher levels.

Importantly, risk appetite is not about encouraging reckless behavior. It is about enabling alignment. When leaders, managers, and teams share a common understanding of acceptable risk, decisions become faster, more consistent, and better aligned with strategic objectives. In modern enterprise risk management, risk appetite serves as a critical bridge between strategy and action. It provides a reference point for prioritizing risks, selecting risk responses, and evaluating trade-offs—ensuring that the organization is neither paralyzed by fear nor exposed by unchecked risk-taking.

8. Risk Appetite vs. Risk Tolerance

Risk appetite and risk tolerance are closely related, but they serve different purposes.

- Risk appetite describes the overall amount and type of risk an organization is willing to accept in pursuit of its objectives. It is strategic in nature and typically set by senior leadership or the board. Risk appetite provides direction and intent—it establishes the organization's general posture toward risk-taking.

- Risk tolerance, on the other hand, defines the acceptable level of variation around specific objectives, risks, or performance measures. It is more operational and is often expressed in measurable terms, such as thresholds, limits, or ranges. Risk tolerance translates risk appetite into practical boundaries that guide day-to-day decisions.

Put simply, risk appetite sets the tone, while risk tolerance sets the limits. Appetite answers "How much risk are we comfortable with?" Tolerance answers "How much deviation is acceptable before action is required?"

Clear alignment between risk appetite and risk tolerance helps ensure that strategic intent is consistently reflected in operational decisions—reducing surprises, improving accountability, and supporting more confident risk-taking.

9. The Risk Management Process in 5 Steps

While organizations may use different terminology or frameworks, most effective risk management approaches follow a common, practical process. At its core, risk management is a continuous cycle of five steps.

Step 1 - Identify Risks

The first step is to identify the uncertainties that could affect the organization's ability to achieve its objectives. This includes both downside risks and potential opportunities. Risks may emerge from internal operations, external forces, strategic decisions, or changes in the broader environment. The goal at this stage is breadth—ensuring that important risks are visible, not yet perfectly defined.

Step 2 - Assess Risks

Once risks are identified, the next step is to understand them. This typically involves assessing the likelihood that a risk might occur and the impact it would have if it did. Some organizations use qualitative ratings (such as low, medium, or high), while others use quantitative measures. The purpose is not precision for its own sake, but prioritization—distinguishing which risks matter most.

Step 3 - Prioritize Risks

Not all risks deserve the same level of attention. Prioritization helps focus time, resources, and leadership attention on the risks that could most significantly influence outcomes. This step often considers the impact of risks on key objectives, as well as risk appetite—helping organizations decide which risks are acceptable and which require action.

Step 4 - Treat Risks

Risk treatment involves deciding what to do about prioritized risks. Options typically include accepting the risk, reducing it, transferring it (for example, through insurance or contracts), or avoiding it altogether. Importantly, treatment decisions should align with strategy and risk appetite—balancing potential upside against downside exposure. Treating risks often includes creating, assigning, and following up on action plans.

Step 5 - Monitor and Review

Risks and assumptions change over time. The final step is to monitor key risks, track indicators, and review whether risk responses remain effective. This step closes the loop and ensures that risk management remains relevant, forward-looking, and embedded in ongoing decision-making.

Taken together, these five steps transform risk management from a one-time exercise into a living process—one that helps organizations navigate uncertainty, adapt to change, and pursue objectives with greater confidence.

10. Risk Treatment Explained

Risk treatment is the step where analysis turns into action. Once risks have been identified, assessed, and prioritized, organizations must decide how they want to respond.

There is no single "correct" response to every risk. Instead, risk treatment involves making deliberate choices that align with strategy and risk appetite. In practical terms, organizations typically follow one or more of the following approaches. Each option comes with trade-offs in cost, complexity, and opportunity.

- Accept – Acknowledge the risk and take no additional action because it falls within the organization's risk appetite or the cost of mitigation outweighs the benefit.

- Reduce (Mitigate) – Take actions to lower the likelihood and/or impact of the risk, such as improving processes, adding controls, or increasing preparedness.

- Transfer – Shift some or all of the risk to another party, typically through insurance, contracts, or outsourcing arrangements.

- Avoid – Eliminate the risk entirely by choosing not to pursue the activity or by changing plans, scope, or objectives.

Importantly, treating a risk does not always mean trying to eliminate it. In many cases, the most effective response is to consciously accept a level of risk because the potential rewards outweigh the downsides. The goal of risk treatment is not zero risk, but well-understood and well-managed risk.

Strong risk treatment decisions are informed by context. They consider how a risk interacts with other risks, how it affects objectives, and how resilient the organization would be if the risk materialized.

11. Rating and Scoring Risks

Once risks have been identified, they need to be rated and scored so they can be compared, prioritized, and managed consistently. Rating risks helps organizations move from a long list of uncertainties to a clear view of which risks matter most.

Most organizations rate risks using two core dimensions:

- Likelihood – the probability that the risk will occur

- Impact – the magnitude of the effect on objectives if it does occur

These dimensions are often assessed using simple qualitative scales (for example, low, medium, high) or numeric scales (such as 1 to 5). The intent is not to predict the future with precision, but to apply structured judgment in a consistent way.

In the field of enterprise risk management, 1-5 ratings are most commonly used, as follows:

| Likelihood | Impact |

|---|---|

| 1 - Rare | 1 - Insignificant |

| 2 - Unlikely | 2 - Minor |

| 3 - Possible | 3 - Moderate |

| 4 - Likely | 4 - Major |

| 5 - Almost Certain | 5 - Extreme |

Likelihood and impact scores are commonly combined to produce an overall risk rating. This allows risks to be plotted on a risk matrix (heat map) or ranked in a prioritized list. Higher-rated risks receive more attention, while lower-rated risks may simply be monitored or accepted.

Good risk scoring practices emphasize clarity and consistency over complexity. Clear definitions, examples, and guidance help ensure that different people across the organization interpret likelihood and impact in roughly the same way. This helps to standardize risk scores across the organization, making risk discussions more meaningful and supporting better decision-making.

A best practice employed by many risk managers is to provide instructions to the business people doing the rating that include examples relevant to their organization and broken down by risk category. This allows risk raters to use their business judgement while following a standardized and easy-to-interpret rating scale. See our article on the Risk Assessment Matrix for examples of these instructions.

Importantly, risk scores are not static. As conditions change, controls improve, or new information becomes available, risk ratings should be revisited and updated.

12. Inherent Versus Residual and Target Risk

When rating risks, it is helpful to distinguish between inherent risk, residual risk, and target risk. These concepts provide important context for understanding how risk changes over time and how effective risk management actions really are.

- Inherent risk is the level of risk that exists before any controls or mitigation actions are applied. It reflects the natural exposure associated with an activity, decision, or environment. For example, operating in a highly regulated industry or launching an innovative product may carry high inherent risk by nature.

- Residual risk is the level of risk that remains after existing controls and mitigation measures are taken into account. This represents the organization's current, real-world exposure. Residual risk is often the most important view for day-to-day management and oversight.

- Target risk (sometimes called desired or acceptable risk) is the level of risk the organization is aiming for, based on its risk appetite and strategic objectives. It represents where leaders want the risk to be over time—not necessarily zero, but within agreed boundaries.

Comparing these three perspectives is powerful. It helps organizations answer practical questions such as:

- Are current controls effective enough?

- Is residual risk aligned with our risk appetite?

- Do we need additional actions to move risk closer to our target level?

In mature risk management practices, the goal is not to eliminate all inherent risk, but to actively manage residual risk toward an agreed target—supporting informed risk-taking while maintaining resilience and control.

13. Example Risk Mitigation Approaches

Risk mitigation refers specifically to actions taken to reduce the likelihood or impact of a risk. Effective mitigation does not eliminate uncertainty, but it does make outcomes more predictable and manageable. Common mitigation approaches include:

- Process improvements

These reduce risk by making work more consistent and less error-prone. Examples include standardizing critical workflows, introducing approval checkpoints, automating manual steps that are prone to mistakes, implementing segregation of duties, or adding quality assurance reviews at key stages.

- Technology solutions

Technology can both prevent incidents and limit their impact. Examples include cybersecurity controls such as multi-factor authentication and intrusion detection, system monitoring and alerting, data backups and redundancy, access controls, and automation tools that reduce reliance on manual intervention.

- Training and awareness

Many risks have a strong human component. Targeted training can reduce the likelihood of errors and improve responses when incidents occur. Examples include cybersecurity awareness training, safety training, scenario-based decision exercises, onboarding programs, and regular refreshers for high-risk roles.

- Policies and procedures

Clear policies help set expectations and guide consistent behavior. Examples include information security policies, procurement and vendor management procedures, incident response plans, escalation protocols, and documented roles and responsibilities for risk ownership.

- Contracts and insurance

Some risks can be partially transferred to third parties. Examples include insurance coverage, indemnification clauses, service level agreements, warranties, and contractual requirements that define responsibilities, liabilities, and performance standards.

Effective mitigation focuses on root causes, not just symptoms. It also considers cost and proportionality—over-controlling low-impact risks can be just as damaging as under-controlling critical ones. The goal is to apply the right level of mitigation in support of objectives and risk appetite.

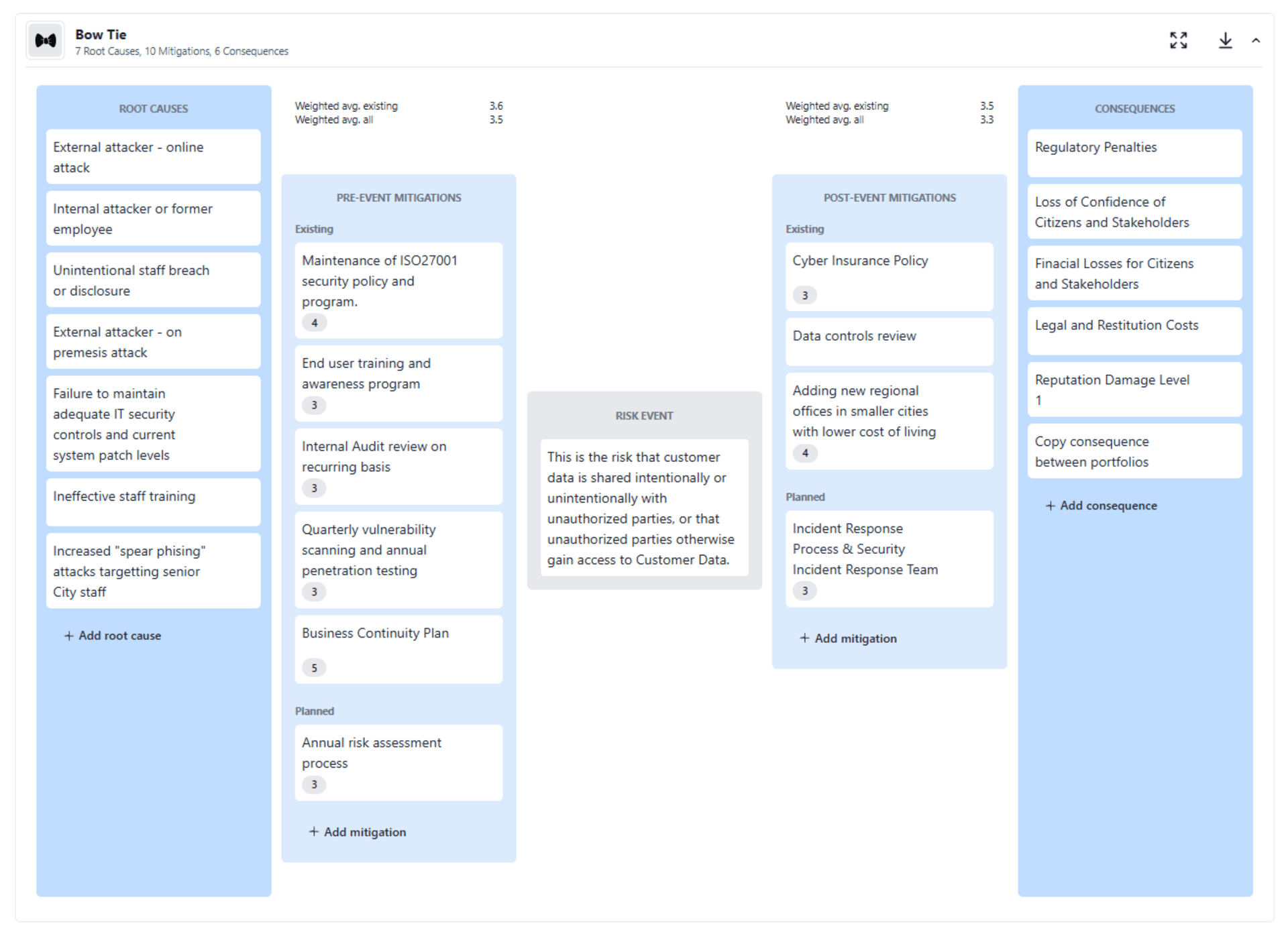

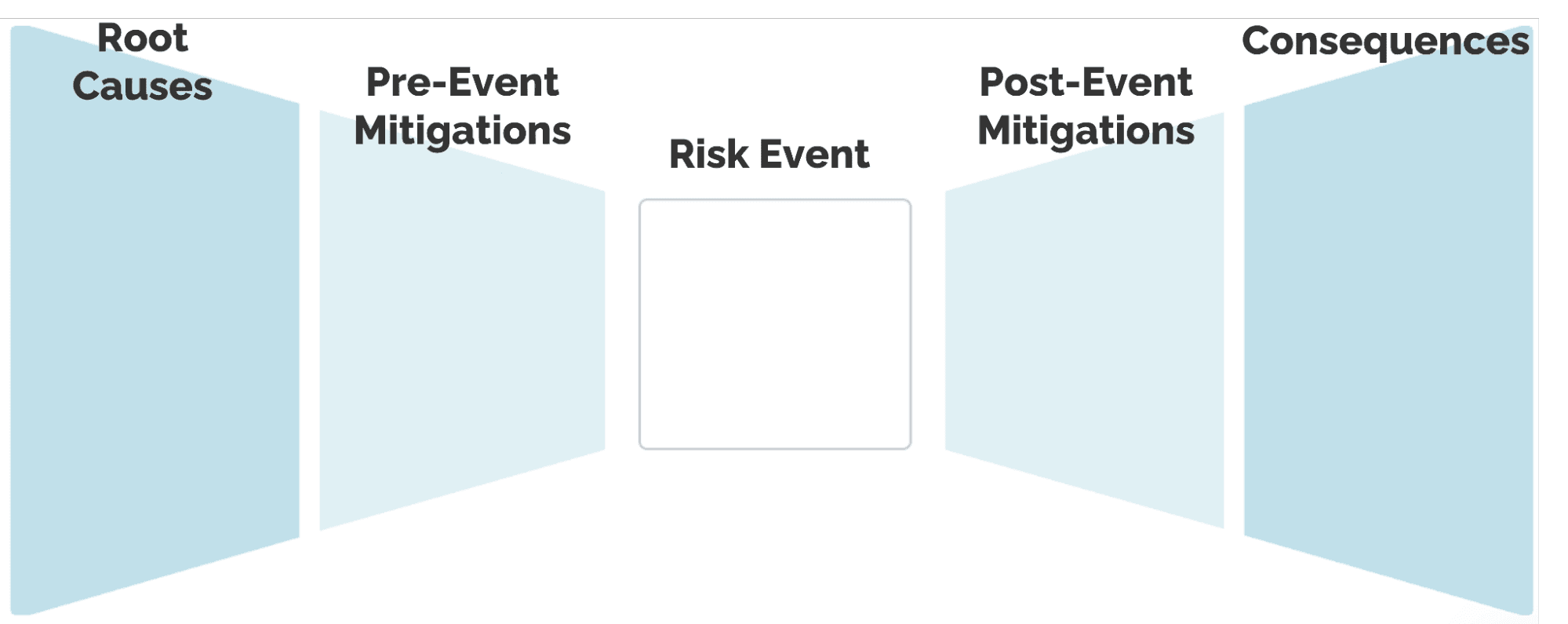

A particularly effective way to design mitigation strategies is the bow tie method. Bow tie analysis visually maps a risk from causes (threats) on the left, through the risk event, to consequences on the right. This structure makes it easy to identify preventive controls that reduce the likelihood of the event and mitigating controls that reduce the impact if it occurs. Bow ties are especially valuable for complex, high-impact risks because they can map multiple scenarios that flow from left to right, in a single, intuitive view.

🎯 Try Our Risk Bow Tie Tool

Map scenarios and controls with our interactive bow tie diagram builder

Open Bow Tie Builder📊 Try Our Risk Matrix Tool

Create, score, and visualize risks with our interactive risk matrix template

Open Risk Matrix Tool

14. Eight Key Elements of a Risk Framework

A risk framework is the practical blueprint that explains how risk management works inside an organization. It turns high-level intent—such as "we manage risk well"—into clear, repeatable actions that people can actually follow.

In practice, a risk framework typically defines what risks are, how they are assessed, who is responsible, and how risk information is used in decisions. While frameworks vary by organization, most mature risk frameworks include the following core elements.

1. Risk Categories and Taxonomy

Most frameworks define a small number of top-level risk categories (such as strategic, operational, financial, and compliance) along with more detailed sub-categories. This provides a shared language and helps ensure risks are identified consistently across departments. For example, "cyber risk" might be a sub-category under operational risk, while "regulatory change" might sit under compliance risk.

2. Risk Definitions and Guidance

Frameworks usually include clear definitions and examples to help people understand what qualifies as a risk and how to describe it. This guidance reduces ambiguity and improves the quality of risk information, especially when risks are identified by non-experts across the organization.

3. Risk Assessment Methodology

A framework defines how risks are assessed, including:

- What likelihood and impact mean in practical terms

- Whether assessments are qualitative, quantitative, or both

- The scales used (for example, low to high, or numeric ranges)

- How inherent risk, residual risk, and control effectiveness are considered

This ensures that risks are evaluated consistently and can be meaningfully compared and prioritized.

4. Risk Appetite and Tolerance Alignment

Most frameworks explain how risk appetite and risk tolerance are applied in practice. This might include thresholds, escalation triggers, or guidance on when risks must be actively managed, reported, or accepted by senior leadership.

5. Roles and Responsibilities

A risk framework clearly defines who does what. This often includes:

- Who identifies and owns risks

- Who assesses and updates them

- Who approves risk treatments

- Who oversees risk at the executive or board level

Clear accountability is essential to prevent risks from being ignored or falling between organizational silos.

6. Risk Treatment and Response Guidance

Frameworks typically outline the available risk treatment options—accept, reduce, transfer, or avoid—and provide guidance on when each may be appropriate. This helps ensure risk responses are deliberate, proportionate, and aligned with strategy.

7. Reporting, Escalation, and Governance

Most frameworks specify how risks are reported, how often they are reviewed, and when they must be escalated. This may include regular risk reviews, dashboards, key risk indicators, and defined governance forums where risks are discussed and decisions are made.

8. Integration with Strategy and Operations

Modern risk frameworks explicitly connect risk management to strategic planning, budgeting, projects, and performance management. Rather than operating as a standalone process, risk becomes part of how decisions are evaluated and trade-offs are made.

15. Common Mistakes to Avoid in Risk Management

Even well-intentioned risk management efforts can fall short if they become disconnected from how the organization actually operates. Some of the most common pitfalls include:

Not establishing clear governance and ownership

Risk management fails quickly when it is unclear who owns a risk, who is responsible for action, and who has authority to accept or escalate it. Without defined ownership and governance, risks can become "everyone's problem" which often means no one's. Alternatively, a situation may develop where risks are seen as the problem or the risk manager, rather that the true business owners.

Making the process too complex

Overly detailed models, excessive scoring criteria, or dense documentation can discourage participation and reduce the quality of inputs. If risk management is not practical and actionable, it will be bypassed. Simplicity almost always outperforms sophistication. We've never seen the roll-out of a risk management program fail because it was too simple, but many well intentioned risk managers have set their efforts back with an "elegant" or overcomplicated program that business users failed to embrace.

Falling in love with terminology instead of outcomes

Organizations sometimes spend too much time debating definitions, labels, and frameworks, and not enough time discussing what the risks actually mean for objectives and decisions. Shared language matters—but only insofar as it supports better conversations and choices. Similarly, risk managers can sometimes be too rigid in their terminology, rather than being flexible to incorporate terminology that may be more intuitive or aligned with their company's business language. Getting user buy-in is more important than always using the "right" risk terms.

Inadequate change management

Introducing risk management as a new process or tool without explaining why it matters or how it helps people do their jobs often leads to resistance or passive compliance. Effective risk management requires communication, leadership support, and reinforcement over time. And when rollout out risk management automation technology, providing process training (that just happens to include the new technology) that is geared to end-user personas is critical for success.

Falling in love with your spreadsheet

Spreadsheets are useful starting points, but they can quickly become brittle, outdated, and difficult to scale. When risk management becomes a static reporting exercise rather than a living process, it loses relevance. The focus should be on insight and action, not just documentation. Modern risk management tools, like our Essential ERM system, come preconfigured to best practice frameworks (e.g. ISO 31000) and ready to use on day one, making them faster and easier that spreadsheets—and exponentially easier to scale and support.

Treating risk management as a one-time exercise

Risks evolve. Assumptions change. Organizations that only review risks annually or after incidents are often reacting too late. Risk management works best when it is continuous and integrated into regular decision-making.

Avoiding these common mistakes helps ensure that risk management remains relevant, trusted, and genuinely useful to leaders and teams.

16. Why is Risk Management Different in 2026?

Risk management in 2026 looks very different from the risk management of even a decade ago.

Organizations are operating in an environment defined by faster change, greater interconnectedness, and higher uncertainty. Artificial intelligence, digital platforms, rapidly changing international norms and alliances, climate impacts, regulatory expansion, and shifting workforce expectations have made risks more dynamic and less predictable. Single events can cascade quickly across operations, finances, reputation, and strategy.

As a result, modern risk management is increasingly forward-looking and decision-focused. It is less about static risk registers and more about understanding scenarios, trade-offs, and resilience. Leaders want timely insight into what could materially affect outcomes—not just a catalogue of past issues.

Risk management in 2026 is also more integrated. It connects strategy, projects, performance, compliance, and operations, rather than sitting in a separate silo. Risk information is expected to inform planning, investment decisions, and prioritization in real time.

Finally, technology has changed expectations. Risk leaders are moving away from manual, spreadsheet-driven processes toward systems that support collaboration, visualization, automation, and continuous monitoring. The goal is not to eliminate uncertainty, but to navigate it with clarity and confidence.

In this environment, organizations that treat risk management as a strategic capability—rather than a reporting obligation—are better positioned to adapt, compete, and thrive.

17. Ready to Manage Risks?

Understanding risk is the first step. Turning that understanding into consistent, actionable practice is where many organizations struggle.

Tracker and our partners help organizations move quickly from concepts to execution. We work with clients to establish practical risk frameworks, clarify risk appetite, and embed risk management directly into strategy, planning, and day-to-day decision-making—all without unnecessary complexity.

Our award-winning platform supports strategy planning and execution, enterprise risk management, regulatory and IT compliance, third-party risk management, and more—all in one integrated system designed for real-world use, not theory.

If you're ready to manage uncertainty with greater confidence—and use risk management as a tool to achieve your goals rather than slow them down—we'd be happy to talk.

Ready to Implement Professional Risk Management?

See how Tracker Networks can help you build and manage effective risk management programs with our comprehensive GRC platform.

_BestMeetsRequirements_Mid-Market_MeetsRequirements.svg)

_BestSupport_Enterprise_QualityOfSupport.svg)

_BestSupport_Mid-Market_QualityOfSupport.svg)

_BestSupport_QualityOfSupport.svg)

_BestUsability_Mid-Market_Total.svg)

_EasiestAdmin_EaseOfAdmin.svg)

_EasiestAdmin_Enterprise_EaseOfAdmin.svg)

_EasiestAdmin_Mid-Market_EaseOfAdmin.svg)

_EasiestSetup_EaseOfSetup.svg)

_EasiestSetup_Mid-Market_EaseOfSetup.svg)

_EasiestToDoBusinessWith_EaseOfDoingBusinessWith.svg)

_EasiestToDoBusinessWith_Enterprise_EaseOfDoingBusinessWith.svg)

_EasiestToDoBusinessWith_Mid-Market_EaseOfDoingBusinessWith.svg)

_EasiestToUse_Enterprise_EaseOfUse.svg)

_EasiestToUse_Mid-Market_EaseOfUse.svg)

_FastestImplementation_Mid-Market_GoLiveTime.svg)

_HighPerformer_Enterprise_HighPerformer.svg)

_HighPerformer_HighPerformer.svg)

_HighPerformer_Mid-Market_HighPerformer.svg)

_HighestUserAdoption_Mid-Market_Adoption.svg)

_MostImplementable_Mid-Market_Total.svg)

_UsersMostLikelyToRecommend_Mid-Market_Nps.svg)